Clarity for Life’s Key Decisions

Ideasager turns complexity into clear, data-driven choices.

As Chen Haoran, I dissect how your down payment and loan term fundamentally influence monthly mortgage payments and total cost....

Buying a home often feels like it all boils down to one question: “Can I afford the monthly payment?” While that’s certainly important, it’s just the tip of the iceberg. The decisions you make about your down payment and loan term actually kick off a much deeper financial game – one that involves leverage, time, and your long-term wealth. These aren’t just one-off transactions; they’re strategic choices that will shape your financial future for decades to come.

It’s easy to feel overwhelmed by the classic dilemma: should you push for a bigger down payment, or go for a shorter loan term? Many aspiring homeowners grapple with these long-term implications. My goal here is to cut through that complexity. I want to share five crucial insights into how these two key factors – your down payment and loan term – impact both your monthly mortgage payments and the total cost of your home, so you can make truly informed decisions with confidence.

The down payment is essentially your initial investment in your home – your equity stake. Think of it this way: the more cash you put down upfront, the less money you actually need to borrow. This is why a larger down payment directly lowers your loan principal, which then has a ripple effect. It reduces your monthly payments and significantly cuts down the total interest you’ll pay over the life of the loan. It’s one of the simplest, yet most powerful, forms of financial leverage in home buying.

However, there’s a common trap many fall into: over-extending themselves for a huge down payment. While a lower monthly payment sounds great, draining your emergency savings or selling off other valuable assets that could be growing elsewhere might not be the smartest move. The real wisdom lies in finding that sweet spot, balancing the desire for a lower mortgage payment with your need for financial liquidity and other smart investment opportunities.

Now, let’s talk about the loan term – this is simply how long you have to pay back your mortgage. This choice profoundly impacts your monthly budget and your overall financial freedom. Opting for a shorter term, like 15 years, usually means you’ll pay significantly less in total interest over the life of the loan. Why? Because you’re paying off the principal much faster, giving less time for interest to accumulate. The trade-off, though, is substantially higher monthly mortgage payments.

On the flip side, a longer term, say 30 years, gives you the benefit of lower monthly payments. This can free up valuable cash flow, giving you more flexibility for other financial goals or unexpected expenses. But remember, this flexibility comes at a price: you’ll end up paying considerably more in total interest over the long haul. For example, a $300,000 loan at 4% interest could rack up about $215,000 in total interest over 30 years. Shorten that to 15 years, and the total interest might drop to around $99,000. This striking difference really underscores the explicit cost of time when you borrow for a mortgage.

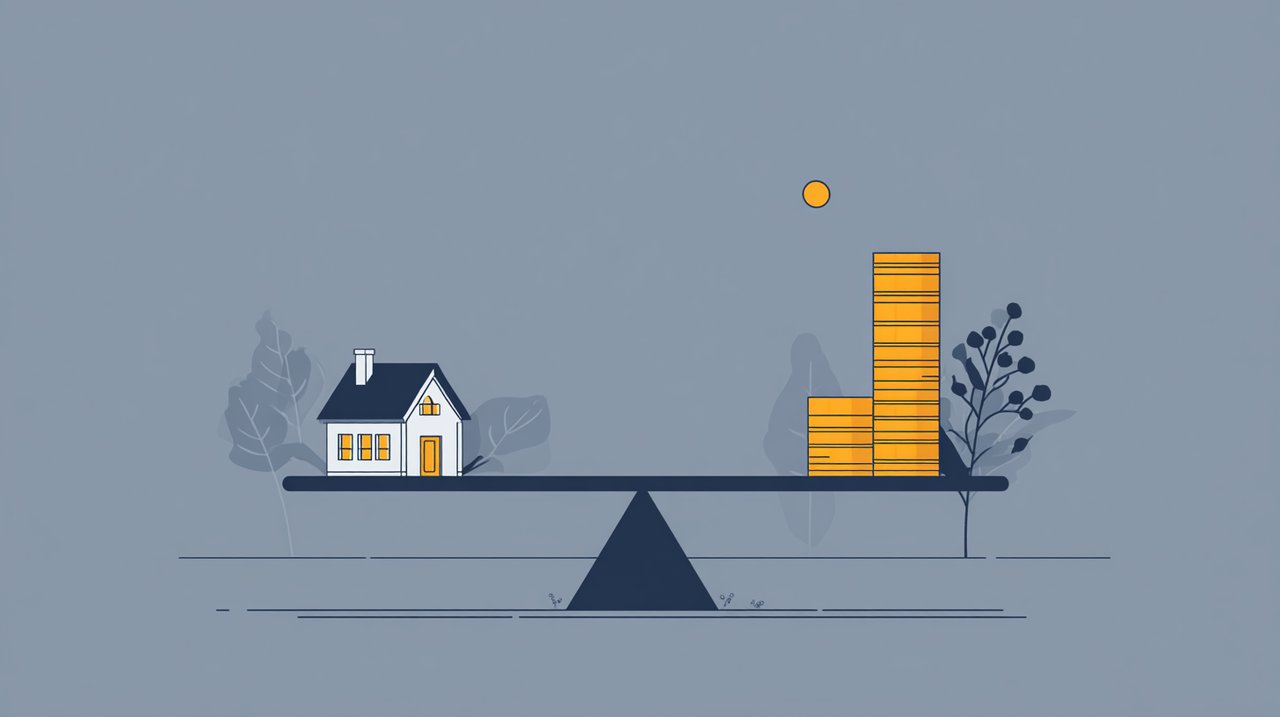

It’s crucial to understand that your down payment and loan term aren’t isolated decisions; they’re deeply interconnected. Think of it like a financial seesaw, balancing your monthly payments against the total cost of your mortgage. A larger down payment can effectively lighten one side, easing the burden of those monthly payments. Or, you could pair it with a shorter loan term to dramatically reduce the total interest you’ll pay.

Let’s consider a practical example for a $400,000 home. Imagine the difference between a 10% down payment with a 30-year term, versus a 20% down payment with a 15-year term. These two scenarios will present vastly different pictures, both for your monthly outlay and the ultimate cost of your home. This is precisely where an online mortgage payment calculator becomes your best friend, letting you plug in different combinations to discover your optimal balance point (you can utilize our dedicated tool to precisely calculate your mortgage payments Mortgage Calculator). The real aim here is to craft a strategy that comfortably supports your current cash flow, without sacrificing your long-term financial well-being.

“Financial wisdom lies not in minimizing every cost, but in optimizing the flow of capital to achieve your grandest goals.”

First-time buyers often face a unique tightrope walk: how do you balance immediate affordability with your long-term financial growth? You’re typically working with limited capital and perhaps a less predictable income. So, the initial decision around how your down payment affects your mortgage payments becomes absolutely critical. A smaller down payment might open the door to homeownership, which is great, but it often means higher monthly payments, partly due to private mortgage insurance (PMI) and a larger principal loan amount.

For many, it makes smart sense to initially opt for a longer loan term. This keeps those monthly payments more manageable, freeing up crucial cash flow. You can then strategically pair this approach with future plans, perhaps making extra principal payments as your income grows, or refinancing when market conditions are more favorable. A common misstep we see is stretching every last dollar for the biggest possible down payment, which can leave you with no financial buffer for unexpected expenses or valuable investment opportunities.

Let’s move beyond just the numbers for a moment. The true heart of smart mortgage decision-making lies in grasping the profound concept of time value. From this strategic viewpoint, your mortgage isn’t just a debt you need to chip away at; it’s a powerful financial instrument. When you leverage low-interest mortgage debt, particularly in an environment where inflation is at play, the real value of your fixed payments actually shrinks over time. This effectively reduces the true cost of your borrowing.

This perspective brings us to a fundamental philosophical question: Is it always best to aggressively pay off your mortgage, or should you strategically use that low-cost debt to invest your capital elsewhere, aiming for potentially higher returns? Historically, well-diversified investment portfolios have often delivered returns that outpace typical mortgage interest rates. This means that the opportunity cost of quickly paying down a low-interest mortgage could be substantial, potentially causing you to miss out on significant wealth accumulation in other areas. This insight is truly at the core of any mortgage loan term comparison when you view it through a strategic wealth-building lens, rather than simply as a way to minimize costs.

“The greatest financial leverage is not just borrowing wisely, but understanding what your money can do for you over time.”

Ultimately, navigating your mortgage choices is a deeply personal journey – a dynamic interplay of financial leverage and the cost of time. There’s no single “best” approach that fits everyone. Instead, the goal is to find the strategy that aligns perfectly with your unique financial situation, your risk tolerance, and your long-term aspirations. Having a solid grasp of how your down payment affects mortgage payments and the subtle nuances of comparing different mortgage loan terms is truly indispensable.

I strongly encourage you to use a monthly mortgage payment calculator to run various scenarios tailored to your specific circumstances. Even more importantly, consider reaching out to a trusted financial advisor. Their objective expertise can provide that nuanced perspective you need to transform these insights into a robust, actionable financial plan, ultimately setting a sturdy foundation for your long-term wealth. This way, you’re not just buying a house; you’re strategically building your future, just as we discussed at the beginning.

A larger down payment reduces the amount you need to borrow, which directly leads to lower monthly payments and significantly less total interest paid over the life of the loan. However, it's important not to over-extend by draining emergency savings or other valuable assets.

A shorter loan term (e.g., 15 years) typically results in higher monthly payments but much less total interest paid over time. A longer loan term (e.g., 30 years) offers lower monthly payments, providing more cash flow flexibility, but you will pay considerably more in total interest over the life of the loan.

This strategic viewpoint considers mortgage debt as a financial instrument. It suggests that the real value of fixed mortgage payments can shrink over time due to inflation, effectively reducing the true cost of borrowing. This perspective encourages evaluating whether to aggressively pay off a mortgage or strategically invest capital elsewhere for potentially higher returns.

First-time buyers often face limited capital. A smaller down payment might be necessary to achieve homeownership, but it can lead to higher monthly payments (potentially including private mortgage insurance). It's often smart to initially opt for a longer loan term for manageable monthly payments, then make extra principal payments or refinance as income grows or market conditions improve.

It's recommended to use an online mortgage payment calculator to compare different scenarios tailored to your circumstances. Additionally, consulting a trusted financial advisor can provide objective expertise to help you create a robust financial plan that aligns with your unique situation and long-term aspirations.